Getting your finances right is essential if you are looking to get your business off the ground. There are multiple ways for you to get the funding you need. The real question then would be, which option is the right one? For those still trying to figure out how to start a business, this can be somewhat overwhelming to answer. This article aims to ease such worries. Take a look at the options listed and determine for yourself what the best choice would be for your business.

Do You Qualify?

Whether you qualify or not is an important question to ask. As much as you may want to just pick and choose funding types, you also need to make sure that you qualify. Prepare yourself, because even though there will be different requirements, there are always things you can do to help your situation. One of these things would be making sure that your credit scores are built up, both professionally and personally. From there, look into the minimum requirements and qualifications of the lender. Gather all the necessary financial and legal documents and develop your business plan. Being able to provide collateral is also a fine way to prepare yourself for qualification.

Choose A Funding Option

If you want to ensure your company’s momentous future, then it is imperative to properly structure your finances. From the beginning, this means finding the funding type that you need best and prefer the most. As an example, there are those that don’t mind equity, but some may be unwilling to barter some control for money. To make the best choices, first develop a solid understanding of what’s on the table.

Decide How Much or When it is Needed

There are two important decisions that you need to make regarding funding. One would be the amount of money that your business will be needing. The second one would be when the money will be needed. It is natural for your circumstance to largely shape your choices, but some tips for both decisions are definitely going to be in order.

-

How Much You Would Need

When launching a startup, a good call to make would be to ask for as little as you need. Despite that, you need to ensure that you aren’t being short-sighted or that you will run out of money before achieving your goals. Speaking of goals, you can also get an idea of how much you’ll need based on them. Establish what you want to accomplish first and then consider your funding.

-

When Do You Need It

There will be various points where you will need funding. You can get help in order to get your business off the ground. Then again, you may need additional funding down the line to keep it afloat. A prototype or a new addition to your product line may need an extra nudge from the outside. All of these instances are perfectly acceptable in times where you will need funding.

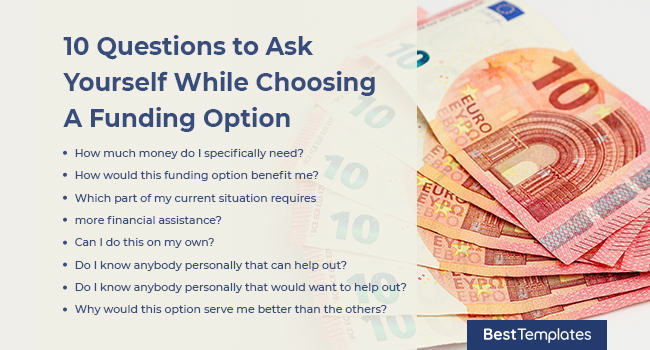

10 Questions to Ask Yourself While Choosing A Funding Option

Asking yourself certain questions whilst you make a decision can help steer you towards a much smarter and better path. When said decision involves choosing a funding option, this becomes incredibly important. Below are ten questions that may be of great use to you as you seek funding for your startup.

- How much money do I specifically need?

- How would this funding option benefit me?

- Which part of my current situation requires more financial assistance?

- Can I do this on my own?

- Do I know anybody personally that can help out?

- Do I know anybody personally that would want to help out?

- Why would this option serve me better than the others?

- How would this choice impact my business in the short-term?

- How would this choice impact my business in the long-term?

- If one fails, which option is the next best thing?

Equity (What is it?)

To put it simply, equity is an asset’s value less all of its liabilities. Many prefer to represent it using the equation of [assets – liabilities = equity]. Even then, it can have differing meanings. Equity in property is common, but so are stocks, which represent ownership within a firm. To determine your business’ equity, you will first need to determine the value. Do this by factoring owned land, capital goods, buildings, earnings, and inventory. Debts and overhead will comprise your liabilities, so it is important to take those into account as well.

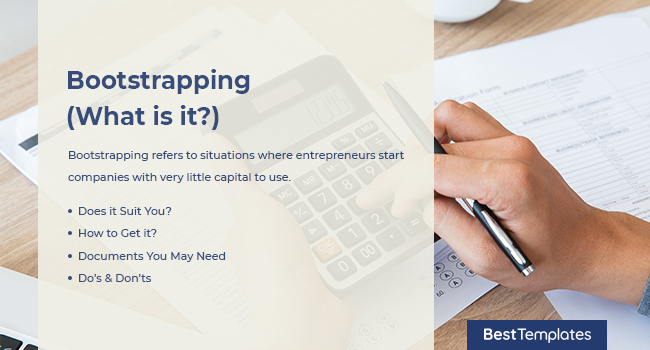

Bootstrapping (What is it?)

Bootstrapping refers to situations where entrepreneurs start companies with very little capital to use. Personal finances may be used as funding or perhaps through the new company’s operating revenues. One major benefit to this would be the fact that entrepreneurs who bootstrap can maintain full control over their decisions. The downside would be risking personal financial disaster on the entrepreneur’s part. It must also be noted that the investment may not be anywhere near enough for the new company to succeed at reasonable rates.

-

Does it Suit You?

There are studies that show how more than 80% of new startups are funded through personal finances. Unless you want to get loans from banks and other institutions, bootstrapping may be an option you’d want to take into consideration.

-

How to Get it?

This is something that you can start on your own. It is a steady way to start compiling revenue for your business, although quick profits should not be expected right away.

-

Documents You May Need

None. A business plan may be in order though, since you are going to be putting your own money to use. You might as well meticulously plan out each step of the way.

-

Do’s & Don’ts

It is advisable to first have a worthy concept or a product in mind before you seek out money. Proceed to pre-sell your idea then project your expenses. Do evaluate as many non-scalable methods and resources possible. Don’t make the mistake of neglecting the grunt work that will be involved in this method of funding.

Self-Funding (What is it?)

This term more or less explains itself. When going down this path, you are solely responsible for funding for your business ventures. Benefits to this include being the owner of your company as a whole, without having to yield equity to outsiders. However, this can also be quite tough if your capital requirements are large. Plus, accepting funding from others may serve to accelerate your company’s growth in ways that might not always be possible with self-funding.

-

Does it Suit You?

If you are one of those business owners that want to retain full control and ownership of your business, then this is the funding option for you. Should you have enough of your own personal money saved up, then this ought to suit you fine.

-

How to Get it?

You are free to acquire the money meant for self-funding however you see fit. As long as the amount is sufficient in order to achieve your goals.

-

Documents You May Need

There are no documents required for you to be able to fund your company out of your own pocket.

-

Do’s & Don’ts

Do properly estimate just how much you will need as a whole and for specific periods. Don’t be careless with your spending.

Friends & Family (What is it?)

Investments from friends and family are also viable funding options that you can take a look at. In fact, these may be among the most common startup funding forms out there. After all, independent investors and banks may need a lot of convincing, but those closest to you may be more willing to take the financial risk. This is also one of your best chances to secure your much needed money, not to mention they are likely to be much more forgiving with any ups and downs experienced by your business.

-

Does it Suit You?

If you can’t raise money yourself and if approaching other lenders is not an option you want to deal with, then this should be perfect for you.

-

How to Get it?

You can receive this type of funding simply by asking a friend or family members.

-

Documents You May Need

To help convince friends and family members, you may need to craft a business plan. You may also want to put your deals with them in writing, as a precaution and to show that you are serious about being professional about this venture.

-

Do’s & Don’ts

Do make sure that you put it all on paper and make the document as detailed as possible. Don’t allow your personal relationships to suffer because of your business relationship. Emphasize that nothing in this is personal and do establish trust going forward. Also make sure that you make your company’s progress as transparent as you can.

Angel Investors (What is it?)

These are the investors that focus more on small startups and entrepreneurs. Usually, these guys are one of the entrepreneur’s friends and family members. What they provide can be in the form of one-time investments or it could be done through ongoing money support. The latter can be quite helpful for when the company goes through its difficult early stages. It should be noted that angel investors tend to provide much more favorable terms in comparison to other types of lenders.

-

Does it Suit You?

If self-funding and going to family and friends for aid are off the table, then perhaps this option may be for you.

-

How to Get it?

There was a time when angel investors were difficult to find. Now there are groups that arrange for meetings with such folk in multiple places. All you have to do is sign up then pay a small fee so you can attend events where entrepreneurs can meet with potential angel investors and VCs.

-

Documents You May Need

Same with family and friends, you’ll need a business plan all sorted out. This will prove to potential investors that you’ve got things figured out. A Memorandum of Understanding can also apply to this situation.

-

Do’s & Don’ts

Doing some research on the investors would be a pretty good idea. Expecting to get funding right away may not be, though. Do make sure to network extensively and please treat your first encounter as step one into a long and fruitful business relationship. Lastly, do not neglect your long-term plans for the business.

Partners (What is it?)

Having a partner means having somebody else to share the numerous burdens and responsibilities. Naturally, this would include the funding for the company. This means providing only half of the amount or a certain portion if your partnership involves more than two people. Even though you are engaged in this type of business relationship, you can still go after other forms of funding options, such as crowdfunding or venture capital.

-

Does it Suit You?

Some may not want to shoulder all the responsibilities alone, so this would be an excellent way to get things done with like-minded people.

-

How to Get it?

Funding with partners can be similar to funding your startup on your own. The only difference here is that there’s another person. You may have different ways of getting your share of the capital, but pooled together, it is for the same cause.

-

Documents You May Need

A business plan is a required document to not only serve as a guideline for you, but to entice others that may want to partner up for your venture.

-

Do’s & Don’ts

Do take the time to carefully consider whom you enter into a business with. Do ensure that you both share the same vision and take care to draw clear lines. Don’t neglect communication. It is as important in business as in any other type of relationship.

Venture Capital (What is it?)

This is the form of financing that sees investors provide aid to those startups that they feel has the most potential for long-term growth. Venture capitalists tend to be either well-off investors or financial institutions such as investment banks. Not only is monetary aid given, but other forms of benefits may be given, such as consultation, mentoring, or in the form of much needed supplies and equipment. Despite the risks for the investors themselves, the allure of above-average returns is what drives them the most.

-

Does it Suit You?

Startups who get venture capital operate on rarified field. If your company isn’t one that looks to grow fast and big, then you aren’t likely to get this type of funding.

-

How to Get it?

Patience is the key when it comes to getting venture capital. Approach select VC firms carefully. Seek out introductions as you cultivate business connections. You may try to seek them out through the firms’ websites, but this ought to be done only as a last resort. Chances will be better if you already fit their profile or met one of their partners.

-

Documents You May Need

A prepared business plan is always recommended. Another document you may want to prepare would be a one-page summary. Send it as a follow-on email after you’ve been introduced to a VC.

-

Do’s & Don’ts

Do make it a point to research as much as you can about potential investors. Ensure that an emotional connection is established and that you can provide a working demonstration of your product. On the other hand, don’t present your business plan if you don’t have any in-depth discussion on why your customers will use it. Another thing to look out for would be don’t try to answer questions that you don’t have a good answer to. This is not the time or place to bluff.

Crowdfunding (What is it?)

This is where you acquire smaller amounts of money from a large group of individuals in order to finance their new business venture. Social media sites and crowdfunding websites are the best ways for entrepreneurs to reach out to potential investors. However, there can be restrictions and regulations regarding this method. In the United States, there are limits on who can fund new businesses and how much money is allowed to be contributed.

-

Does it Suit You?

Crowdfunding allows multiple people to fund a startup, which creates genuine awareness and investment in your company. If that’s what you are looking for, then it would be reason enough to go for this particular funding option.

-

How to Get it?

Once you’ve made the necessary preparations, you need to find the right platform. There are multiple crowdfunding platforms out there for you to choose from. Sites will allow you to choose between ‘donation only or rewards for contributions’ or ‘all or nothing or keep it all’ types of campaigns.

-

Documents You May Need

First of all, you’ll need a business plan and an executive summary. A Pro forma income statement and pitch deck will also be needed, the former for the list of assets, costs, projections, and revenue. For latter is a powerpoint presentation that guides investors through your startup’s key components.

-

Do’s & Don’ts

It is advisable to pre-campaign so that you can build up as much exposure and interest. However, being greedy is an absolute no-no in this scenario. Don’t ask for more money than what you need. Also, do come up with a proper budget and don’t forget about the taxes that you will be paying.

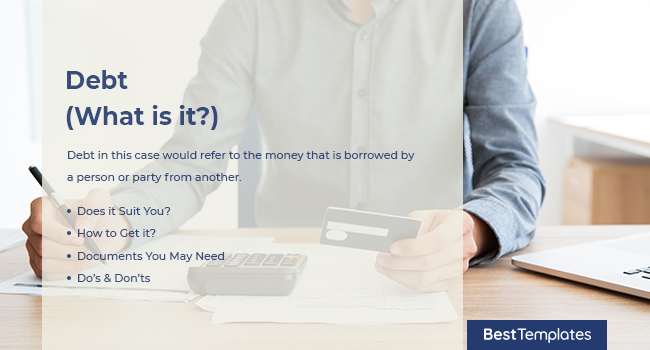

Debt (What is it?)

Debt in this case would refer to the money that is borrowed by a person or party from another. This is utilized by various individuals and corporations as a means of making big purchases that they may not afford under other circumstances. Debt arrangements provides borrowing parties with the permission to borrow under set conditions, such as the date it is to be paid back and how much interest will be involved.

Small Business Lenders (What is it?)

Small business lenders are the non-traditional lenders. What they have to offer will greatly vary; those with bad credit can acquire short-term loans from them, as can those who operate solely online. Unlike other lenders, not only are they willing to provide monetary loans, but they’ll also provide technological help, among others.

-

Does it Suit You?

If you are unable to get loans through traditional bank loans or have difficulty getting loans through other means, then this is for you.

-

How to Get it?

You can get recommendations from others as to where you can find small business lenders. Or you may find them yourself through various methods, such as looking them up online or by networking, and contact them from there.

-

Documents You May Need

Among the documents needed would be your resume, personal background, business plan, credit reports both personal and business, income tax returns, and financial statements. There’s also a need to provide collateral, bank statements, and legal documents.

-

Do’s & Don’ts

Do take the time to look for somebody trustworthy. If you can apply for online loans, then do so as well. Attempting to get multiple loan offers can also be a great idea. However, limit it to just one loan at a time so you won’t extend your debt. Also, do not base choices on just the interest rate. Putting your assets at risk is also not a good idea. SBA

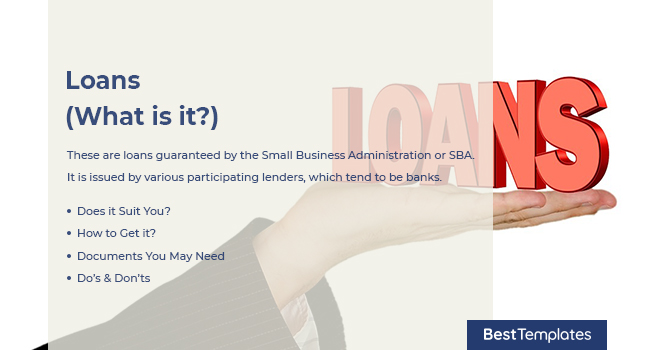

Loans (What is it?)

These are loans guaranteed by the Small Business Administration or SBA. It is issued by various participating lenders, which tend to be banks. Due to the organization’s nature, you can expect higher and more specific requirements than some of the previous options. There may be no restrictions or ceilings, but three criterias for eligibility must be passed. This would include: your net income not surpassing $5 million after taxes for the preceding two years, the project size has to be greater than personal and non-retirement assets, and finally, the company should not possess a tangible net worth in excess of at least $15 million.

-

Does it Suit You?

If your business does not or cannot qualify for traditional bank loans, then this funding method should suit you just fine.

-

How to Get it?

To get a SBA loan, you need to apply and meet the qualifications. First of all, your business needs to be turned down for private funding first. Meeting the size requirements is next. Depending on what loan you’re getting, other criteria may also apply.

-

Documents You May Need

Among the documents you’ll need would be the resumes of company management. Your business plan will also be needed, as will your personal credit report and business credit report. Don’t forget your personal and business income tax returns, financial statements, business debt schedule, and bank statements.

-

Do’s & Don’ts

Do seek out a lender that is SBA-preferred. Make sure that you have your documentation in order and get your financial house together. Don’t, of all things, rule out an SBA loan option. Try not to let the documentation requirements discourage you and definitely do not balk at any request for personal guarantees.

Banks (What is it?)

Banks can be among the largest small business lenders around. For many people, this is the first option that comes to mind when considering loans. A benefit to this is the low loan costs offered. However, it must also be noted that banks can be difficult to qualify for. Applying takes up a lot of time and effort, with the process potentially taking up to three months.

-

Does it Suit You?

There are multiple types of business loans, so choosing the type that suits your business best is what will answer this question. The types include business overdraft, line of credit, secured loan, unsecured loan, fixed rate loan, and variable rate loan.

-

How to Get it?

To get a bank loan, you need to file an application first. From there, you need to compile all the required documents, offer up your collateral, and then outline your agreement with the bank.

-

Documents You May Need

You will need proof of your identity and address, a bank statement, and your latest ITR, along with balance sheet, profit and loss, and income statement of the last two years. A few other mandatory documents will include sole proprietorship declaration and certified true copy of memorandum.

-

Do’s & Don’ts

Do your best to understand what the costs of the loan really is. Make sure that you are aware of any prepayment penalties. If you are unable to pay a loan back, then you need to understand which assets will be at stake. Don’t attempt to close credit card accounts or max out credit cards. Lastly, consolidating your debt must not be attempted.

Quick Comparison

Even with the information stated above, it can still be a bit confusing to choose between numerous options. To help out with the decision making, you may refer to the table below. This compares each option according to certain areas, which will further illustrate their pros and cons.

Filing Requirements

- Bootstrapping – Not much filing needed.

- Self-Funding – Not much filing needed.

- Friends & Family – Not much filing needed.

- Angel Investors – Some filing involved.

- Partners – Not much filing needed.

- Venture Capital – A Lot of Requirements are Needed

- Crowdfunding – Some requirements needed

- Small Business Lenders – Moderate amount of requirements

- SBA Loans – Moderate amount of requirements

- Banks – A lot of requirements are needed

Difficulty of Acquiring

- Bootstrapping – Depends on personal circumstances.

- Self-Funding – Depends on personal circumstances.

- Friends & Family – Depends on personal circumstances.

- Angel Investors – Easy to moderate.

- Partners – Easy to moderate.

- Venture Capital – Can be quite difficult

- Crowdfunding – Easy

- Small Business Lenders -Moderate

- SBA Loans – Moderate

- Banks – Can be quite difficult

Who is Liable

- Bootstrapping – The entrepreneur

- Self-Funding – The entrepreneur

- Friends & Family – The investing friends and family

- Angel Investors – The angel investors

- Partners – The partners

- Venture Capital -The VC firm

- Crowdfunding – The investors

- Small Business Lenders – The lenders

- SBA Loans – The lenders

- Banks – The banks

What Percentage is Worth

- Bootstrapping – 100%

- Self-Funding – 100%

- Friends & Family – Mostly yours

- Angel Investors – Largely yours

- Partners – 50-50 percentage (or less)

- Venture Capital – Varies depending on the seed round

- Crowdfunding – Varies on the circumstances

- Small Business Lenders – Mostly yours

- SBA Loans – Mostly yours

- Banks – Mostly yours

Control

- Bootstrapping – Mostly yours

- Self-Funding – Entirely yours

- Friends & Family – Mostly yours

- Angel Investors – Angel investors are given some equity.

- Partners – Split between partners

- Venture Capital – VC firms gain considerable control

- Crowdfunding – Mostly yours

- Small Business Lenders – Mostly yours

- SBA Loans – Mostly yours

- Banks – Mostly yours

Risk Tolerance

- Bootstrapping – Depends on the entrepreneur

- Self-Funding – Depends on the entrepreneur

- Friends & Family – Low risk

- Angel Investors – Low risk

- Partners – Depends on the partnership

- Venture Capital – Moderate

- Crowdfunding – Low

- Small Business Lenders – Low

- SBA Loans – Low

- Banks – Moderate

How Soon Can You Get it?

- Bootstrapping – As soon as possible

- Self-Funding – As soon as possible

- Friends & Family – As soon as possible

- Angel Investors – Within three to six months

- Partners – As soon as possible

- Venture Capital – Up to six months

- Crowdfunding – As soon as possible

- Small Business Lenders – Two to three months

- SBA Loans – Two to three months

- Banks – A week or so

Easy to Exit?

- Bootstrapping – Yes

- Self-Funding – Yes

- Friends & Family – Moderately

- Angel Investors – Yes

- Partners – Moderately

- Venture Capital – Moderately difficult

- Crowdfunding – Yes

- Small Business Lenders – Moderately

- SBA Loans – Moderately

- Banks – Moderately

Which is Expensive?

- Bootstrapping – Depends on personal circumstances

- Self-Funding – Depends on personal circumstances

- Friends & Family – Depends on personal circumstances

- Angel Investors – Not usually expensive

- Partners – Depends on personal circumstances

- Venture Capital – Can be quite expensive

- Crowdfunding – Depends on personal circumstances

- Small Business Lenders – Depends on personal circumstances

- SBA Loans – Depends on personal circumstances

- Banks – Depends on personal circumstances

Things to Consider When it Comes to Funding

So you think you’ve got everything you need with your present array of funding options. Even with all that, know that there are still a lot to do and look into before you reach the best possible position when it comes to funding. Below are ten considerations that you may want to ponder upon. You may even find that there are things you have not thought about, like what you can do to improve beyond just making a specific funding choice.

10 Things to Consider

- Be on the Lookout for Partnership Opportunities: There are times when partnerships are critical to the success of a venture. This can include finding other means of revenue.

- Be Prepared to Spend a Lot of Time on Fundraising: This is almost a full-time job in its own right. Investor meetings and preparing materials are bound to be incredibly time consuming.

- Thoroughly Understand Your Options: Do your homework and know what you are getting yourself into. Learn to recognize good deals from bad ones. Familiarize yourself with the numerous financial structures and firms that most new to business would be unfamiliar with.

- Don’t Give Away Too Much Equity: Giving away too much equity only serves to lower your options later on. This is something to really think about should you decide to go for venture funding.

- Talk About Your Business Model: If you are unable to talk about it, then how would you be able to discuss your business with potential investors? Discuss your numbers and overall strategy to great lengths if needed.

- Know How You’ll Spend Your Funding: Asking for funding without any idea of how to spend it would be a terrible idea. Be very specific regarding how the money will be used and you are likely to achieve greater success with your business and in acquiring funding in the first place.

- Make Sure You Trust Your Chosen Investors: This should be a given; trust is the foundation of any relationship, be it personal or business. Develop trust between you and your investors, or don’t get involved at all.

- Create an Advisory Board: These things are great due to the fact that they can introduce potential investors to you. In fact, some advisors may even become investors too.

- Build Traction Before Seeking Funding: Ensure that you’ve got a user base or at least revenue traction to justify your funding. This will make the fundraising process a lot easier to do.

- Always Have a Clear Definition of What the Next Level Is: Having a clear idea of future milestones will help you align your funding with any strategies that you’ll need to come up with.

Finances can be tricky, but as you can see, where there is a will, there are multiple ways to choose from. Now that you are better acquainted with the methods involved, you should be better equipped to make funding decisions. Be sure to gather the necessary documents to start a small business regardless of what funding option you choose. It is always better to come prepared for as many opportunities as possible.